The new Democratic House should make worker empowerment a priority

For the first time in nearly a decade, Democrats will hold the majority in the House when Congress convenes in January. The results of yesterday’s election are encouraging and represent historic progress—with a record number of women winning seats in the house, including key victories by diverse candidates across faiths and ethnicities. And importantly, Democrats won the popular vote in the House by a 9.2 percent margin despite today’s 3.7 percent unemployment rate, which should have provide great advantage to the incumbent party.

It is nevertheless important to note that with Republicans in control of the Senate and the White House, it is unlikely that policies that promote a just economy for working people will become law. Still, House Democrats have the opportunity to advance long overdue reforms. It is critical that they focus on an agenda that serves our nation’s workers. This must include House Democrats working to raise workers’ wages, restore workers’ access to justice on the job, and promote workers’ right to collectively bargain.

Workers deserve a fair minimum wage. At $7.25 per hour, the federal minimum wage is now more than 25 percent below where it was in real terms half a century ago. House Democrats must advance legislation to raise the federal minimum wage to $15 per hour by 2024, indexing it to the national median wage thereafter, and phasing out the tipped minimum wage and other subminimum wages. Given inflation expectations, $15 in 2024 would be around $13.00 in 2018 dollars, an appropriate level for the federal floor. The Raise the Wage Act introduced this Congress included all of these reforms. The House must work to pass similar legislation in the new Congress.

Workers should not be forced to sign away their rights as a condition of employment. The use of mandatory arbitration and collective and class action waivers—under which workers are forced to handle workplace disputes as individuals through arbitration, rather than being able to resolve these matters together in court—makes it more difficult for workers to enforce their rights. These agreements bar access to the courts for all types of employment-related claims, including those based on the Fair Labor Standards Act, Title VII of the Civil Rights Act, and the Family Medical Leave Act. This means that a worker who is not paid fairly, discriminated against, or sexually harassed, is forced into a process that overwhelmingly favors the employer—and forced to manage this process alone, even though these issues are rarely confined to one single worker. Congress must act to ban mandatory arbitration agreements and class and collective action waivers. The Restoring Justice for Workers Act introduced this Congress includes all of these reforms. The House should work to pass this important reform in the new Congress.

Voters in Missouri and Arkansas just lifted pay for 1 million workers

In yesterday’s election, voters in Missouri and Arkansas gave overwhelming approval to ballot measures that will raise their state’s minimum wage over the next several years, lifting pay for a combined 1 million workers. In Missouri, 62 percent of voters elected to raise the state minimum wage from its current $7.85 to $12 an hour in 2023. In Arkansas, 68 percent of voters supported a measure that will raise the state minimum wage to $11 per hour in 2021 from its current value of $8.50.

The increase in Arkansas will raise pay for an estimated 300,000 workers (about a quarter of the state’s wage-earning workforce). The Missouri increase will lift pay for 677,000 workers (also about a quarter of wage-earners in the state.) In both cases, the majority of workers who will get a raise are women, most work full time, and they come from families with modest incomes. Analyses of the measures estimate that the raise in Arkansas will put over $400 million into the pockets of low-wage workers there over the course of the increases. In Missouri, low-wage workers will receive nearly $870 million in additional wages over the course of the measure’s implementation.

In voting to raise their state minimum wages, voters in Arkansas and Missouri are making long-overdue corrections to policy failures that political leaders in those states, and at the federal level, should have fixed a long time ago. Raising the minimum wage in Arkansas to $11 by 2021 and $12 by 2023 in Missouri will bring the minimum wage in those states, in both cases, roughly back to where the federal minimum wage was in 1968, when it equaled roughly $10 an hour in today’s dollars. According to the Congressional Budget Office’s (CBO’s) projections for inflation, $11 in 2021 is $9.98 in 2017 dollars, $12 in 2023 is $10.40 in 2017 dollars.

Updating key labor standards, like the minimum wage, is critical if policymakers want to do something about the enormous stagnation in wages that has plagued the country for decades. The recent modest uptick in wage growth is not nearly enough to undo the damage that has been done over the past 70 years. Since the mid-1970s, as the U.S. economy has grown and productivity has risen, hourly pay has barely budged after adjusting for inflation. Since 1973, average labor productivity has grown 77 percent; yet hourly compensation for the typical U.S. worker—and this includes both wages and benefits, such as payments for healthcare premiums and retirement accounts—has grown only 12.4 percent. For low-wage workers, the trends are even worse.

Heading into the midterms, there’s still no evidence that the TCJA is working as promised

It’s been widely reported that going into this year’s elections, Republicans aren’t running on their signature tax law from last year—the Tax Cuts and Jobs Act (TCJA). It’s not difficult to see why. The TCJA is increasingly unpopular, and a recent GOP internal poll shows that respondents say the law benefits “large corporations and rich Americans” over “middle class families.”

Republicans shouldn’t find this so surprising—since the law they wrote was a massive giveaway to the rich and big corporations. And voters do not appear fooled by a PR campaign earlier this year where corporate allies tried to trick workers into believing that any bonus they received in 2017 was due to the TCJA.

The claims of immediate benefits to workers by those corporate allies should never have been taken so seriously by the media. The theory justifying claims that corporate rate cuts should trickle down to typical workers always required that a long chain of economic events to occur first. We’ve long pointed out that nearly every single link in this chain is likely to break down. The first link in this chain concerns firms’ investment; anyone trying to discern if the corporate rate cuts are having their promised effects for workers should be watching investment like a hawk.

The story here doesn’t look any better for proponents of the TCJA than it did in September. The quarterly growth rate in business investment cratered in the third quarter of the year, growing at a 0.8 percent annualized rate. The administration’s favorite data point, the year-over-year increase in real, private nonresidential fixed investment, slowed from 7.1 percent in the 2nd quarter of 2018 to 6.4 percent in the 3rd quarter. Charted below, the data still doesn’t show the clear boost to the trend of investment that would indicate a positive effect coming from the TCJA.

No evidence that the TCJA has increased investment: Year-over-year change in real, nonresidential fixed investment, 2003Q1-2018Q3

| date | NRFI |

|---|---|

| 2003Q1 | -2.3% |

| 2003Q2 | 1.6% |

| 2003Q3 | 4.0% |

| 2003Q4 | 6.8% |

| 2004Q1 | 5.2% |

| 2004Q2 | 4.9% |

| 2004Q3 | 5.7% |

| 2004Q4 | 6.5% |

| 2005Q1 | 9.2% |

| 2005Q2 | 8.2% |

| 2005Q3 | 7.4% |

| 2005Q4 | 6.1% |

| 2006Q1 | 8.0% |

| 2006Q2 | 8.2% |

| 2006Q3 | 7.8% |

| 2006Q4 | 8.1% |

| 2007Q1 | 6.5% |

| 2007Q2 | 7.0% |

| 2007Q3 | 6.8% |

| 2007Q4 | 7.3% |

| 2008Q1 | 5.8% |

| 2008Q2 | 3.8% |

| 2008Q3 | 0.2% |

| 2008Q4 | -7.0% |

| 2009Q1 | -14.4% |

| 2009Q2 | -17.1% |

| 2009Q3 | -16.1% |

| 2009Q4 | -10.3% |

| 2010Q1 | -2.3% |

| 2010Q2 | 4.1% |

| 2010Q3 | 7.5% |

| 2010Q4 | 8.9% |

| 2011Q1 | 8.0% |

| 2011Q2 | 7.3% |

| 2011Q3 | 9.3% |

| 2011Q4 | 10.0% |

| 2012Q1 | 12.9% |

| 2012Q2 | 12.6% |

| 2012Q3 | 7.2% |

| 2012Q4 | 5.6% |

| 2013Q1 | 4.3% |

| 2013Q2 | 2.3% |

| 2013Q3 | 4.4% |

| 2013Q4 | 5.4% |

| 2014Q1 | 5.4% |

| 2014Q2 | 7.6% |

| 2014Q3 | 8.0% |

| 2014Q4 | 6.4% |

| 2015Q1 | 4.5% |

| 2015Q2 | 2.7% |

| 2015Q3 | 0.8% |

| 2015Q4 | -0.7% |

| 2016Q1 | -0.5% |

| 2016Q2 | -0.1% |

| 2016Q3 | 0.8% |

| 2016Q4 | 1.8% |

| 2017Q1 | 4.4% |

| 2017Q2 | 5.3% |

| 2017Q3 | 5.0% |

| 2017Q4 | 6.3% |

| 2018Q1 | 6.7% |

| 2018Q2 | 7.1% |

| 2018Q3 | 6.4% |

Source: EPI analysis of data from table 1.1.6 from the National Income and Product Accounts (NIPA) from the Bureau of Economic Analysis (BEA).

Latina workers have to work 10 months into 2018 to be paid the same as white non-Hispanic men in 2017

November 1 is Latina Equal Pay Day, the day that marks how long into 2018 a Latina would have to work in order to be paid the same wages her white male counterpart was paid last year. That’s just over 10 months longer, meaning that Latina workers had to work all of 2017 and then this far—to November 1!—into 2018 to get paid the same as white non-Hispanic men did in 2017. Put another way, a Latina would have to be in the workforce for 55 years to earn what a non-Hispanic white man would earn after 30 years in the workforce. Unfortunately, Hispanic women are subject to a double pay gap—an ethnic pay gap and a gender pay gap.

The date November 1 is based on the finding that Hispanic women workers are paid 54 cents on the white non-Hispanic male dollar, using the 2016 March Current Population Survey for median annual earnings for full-time, year-round workers. We get similar results when we look at hourly wages for all workers (not just full-time workers) using the monthly Current Population Survey Outgoing Rotation Group for 2017—which show Hispanic women workers being paid 58 cents on the white male dollar.

This gap narrows—but not dramatically—when we control for education, years of experience, and location by regression-adjusting the differences between workers. Using this method, we find that, on average, Latina workers are paid only 66 cents on the dollar relative to white non-Hispanic men.

Yet another reason why Megyn Kelly does not need your sympathy

Megyn Kelly is out at NBC after an uproar over her comments in defense of blackface Halloween costumes during an episode of her television show last week. NBC has canceled “Megyn Kelly Today” and Kelly will be negotiating an exit from her contract. Speculation that Kelly would get a full payout for her three-year, $69 million contract drew a bitter response from people on Twitter. “Congrats to Megyn Kelly for getting $69 million for thinking blackface is fine,” one person tweeted.

Kelly’s unfathomable severance package isn’t the only thing separating her from regular working people. She actually may have a say in her noncompete clause. According to The Hollywood Reporter, her legal representation is “attempting to keep her noncompete clause as short as possible. Six months is the standard in the television news industry.”

Nearly one in five U.S. workers are bound by noncompete agreements, which block them from working for a competitor for a set period of time if they leave their current job. That’s nearly 30 million people who have essentially lost their full right to leave their jobs. And it’s not just highly paid workers who are required to sign them—14.3 percent of workers without a four-year college degree and 13.5 percent of workers earning up to $40,000 a year have noncompetes.

Noncompetes are a big problem. If you are a typical worker and you are not in a union, one of the most important points of leverage you have to negotiate for a raise or fight back against abuse is the fact that you can quit and work somewhere else. A noncompete agreement weakens your power: you have to stay with your employer because you can’t seek or accept a better-paying job with a competitor.

The “boom” of 2018 tells us that fiscal stimulus works, but that the GOP has only used it when it helps their reelection, not when it helps typical families

The Commerce Department released data today on the growth in gross domestic product (GDP—the widest measure of economic activity) in the 3rd quarter of 2018. It showed growth at a 3.5 percent rate in this quarter, down slightly from 4.2 percent growth in the second quarter of 2018. For comparison, in the run-up to the 2016 presidential elections, economic growth had barely averaged 2 percent since recovery from the Great Recession began in mid-2009.

White House economic adviser Larry Kudlow refers to this recent pick-up in growth as the “boom” of 2018. While Kudlow is always hyperbolic and almost always wrong, especially about “booms” (he pronounced in December 2007—the last month before the Great Recession—that “there’s no recession coming. The pessimistas were wrong. It’s not going to happen…. The Bush boom is alive and well.”), it remains worth asking: what is the basis of the faster growth so far in in 2018?

The answer is simple: a pronounced swing from fiscal austerity to fiscal stimulus, enacted by a Republican Congress that decided to help, rather than hurt, the economic recovery once it was being helmed by a Republican president. Yes, that sounds like a harsh and partisan judgement, but it’s the only rational reading of recent years’ evidence.

In the run-up to the 2016 elections, we documented clearly that that recovery from the Great Recession had been intentionally throttled by a historically large dose of austerity; specifically, historically slow growth in public spending. The main actors in imposing that austerity were Republicans in Congress, with some assists from Republican governors and state legislatures (think Sam Brownback from Kansas and Scott Walker from Wisconsin). The quick federal pivot to stimulus once the White House changed hands in 2017 makes the political roots of all this pretty clear.

Six reasons not to put too much weight on the new study of Seattle’s minimum wage

Seattle’s minimum wage increases are one of the most important local policy developments in recent years, but the new study by University of Washington researchers Jardim et al. (2018) is largely uninformative about the effects of the policy because it uses the same flawed methodology that economists criticized in connection with earlier studies by the group. But, even if you believe the results of the new study, a careful reading of its actual findings shows the minimum wage benefited all of the city’s low-wage workers who had jobs prior to the increase.

1. The new study is based on a flawed comparison between Seattle and other areas in Washington state. The comparison causes the study to measure a reduction in the number of new jobs under $15/hour, when in fact this is not a cause for concern.

By comparing workers in Seattle with workers elsewhere in Washington state, the study incorrectly assumes that the low-wage labor market in Seattle would have grown like other areas in Washington, were it not for the city’s 2015-2016 minimum wage increases. This comparison is unreasonable because, as other researchers have demonstrated (Dube 2017, Rothstein and Schanzenbach 2017, Zipperer and Schmitt 2017), Seattle experienced much faster wage gains for reasons that had nothing to do with the minimum wage. Indeed, the authors of the new study find that Seattle had faster wage growth and diverged from other regions prior to the city’s minimum wage increases (see their Table 8 for the 2012-2013 period).

The flawed comparison underlying the study causes it to mistakenly attribute negative employment changes to the minimum wage, when in reality Seattle’s economic boom simply meant that low-wage jobs were converted into higher-wage jobs. For example, the authors document a decline in newly employed workers earning less than $15/hour and argue that the minimum wage is causing “losses in employment opportunities.” Instead, as jobs in Seattle’s tightening labor market were upgraded from lower-wage to higher-wage jobs, there was a mechanical decline in the number of new entrants under any given low-wage threshold. The purported decline in new entrants is not a cause for concern. The fast wage growth in Seattle relative to comparison regions prevents the study from making credible claims about the consequences of the city’s minimum wage increases in 2015 and 2016.

Top 1.0 percent reaches highest wages ever—up 157 percent since 1979

Newly available wage data for 2017 show that annual wages grew far faster for the top 1.0 percent (3.7 percent) than for the bottom 90 percent (up only 1.0 percent). The top 0.1 percent saw the fastest growth, up 8.0 percent—far faster than any other wage group. This fast wage growth for the top 0.1 percent reflects the sharp 17.6 percent spike upwards in the compensation of the CEOs of large firms: executives comprise the largest group in both the top 1.0 and top 0.1 percent of earners. The fast wage growth of the top 1.0 percent in 2017 brought their wages to the highest level ever, $719,000, topping the wage levels reached before the Great Recession of $716,000 in 2007. The wages of the top 0.1 percent reached $2,757,000 in 2017, the second highest level ever, roughly only 4 percent below their wages in 2007.

These are the results of EPI’s updated series on wages by earning group, which is developed from published Social Security Administration data. These data, unlike the usual source of our wage analyses (the Current Population Survey) allow us to estimate wage trends for the top 1.0 and top 0.1 percent of earners, as well as those for the bottom 90 percent and other categories among the top 10 percent of earners. These data are not topcoded, meaning the underlying earnings reported are actual earnings and not “capped” for confidentiality.

What to Watch on Jobs Day: Keeping an eye on the teacher jobs gap

On Friday, the Bureau of Labor Statistics will release September’s numbers on the state of the labor market. As usual, I’ll be paying close attention to nominal wage growth as well as the prime-age employment-to-population ratio, which are two of the best indicators of labor market health. Friday’s report will also give us a chance to examine the “teacher gap”—the gap between local public education employment and what is needed to keep up with growth in the student population.

Thousands of local public education jobs were lost during the recession, and those losses continued deep into the official economic recovery, even as more students started school each year. This has been true of public sector jobs in general—continued austerity at all levels of government has been a drag on public sector employment, which has failed to keep up with population growth.

Teacher strikes in several states over the last couple of years have highlighted deteriorating teacher pay as a critical issue. My colleague Emma Garcia has forthcoming work that further documents shortcomings in the teaching profession today, including important issues of quality, particularly worse in high-poverty schools.

The costs of a significant teacher gap are high, and consequences measurable: larger class sizes, fewer teacher aides, fewer extracurricular activities, and changes to curricula. Last year, the local public education job shortfall remained large. To solve this problem, state and local governments need to fund more teaching positions and raise pay to close the teacher pay gap and attract and retain high quality teachers. On Friday, I will compare where jobs in public education should be, using the pre-recession ratio, student population growth, and the most recent jobs numbers.

The Fed’s current path might be leaving lots of money on the table unnecessarily

Today the Federal Reserve Open Market Committee (FOMC) will almost surely announce it is continuing on its path of steady interest rate hikes. These hikes are meant to start slowing the growth of the U.S. economy in the name of getting ahead of the curve on any potential outbreak of inflation. It’s important to be really clear on this point. The Fed is trying to keep economic growth slower than it would have otherwise been, and unemployment higher than it would otherwise have been, if they had not raised rates.

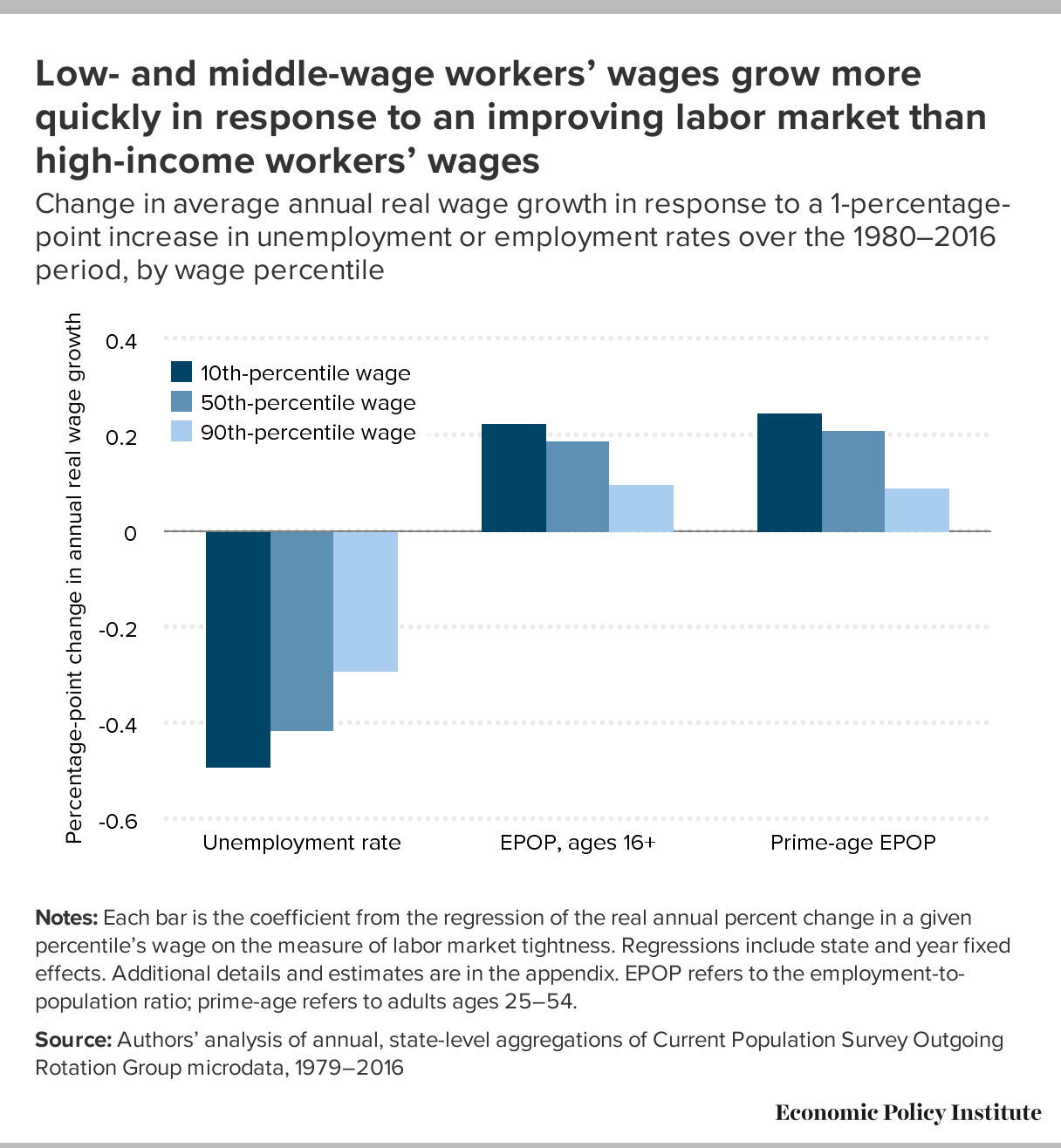

Intentionally keeping unemployment higher than it would have been will strike many as hard to believe—why would the Fed ever do this? The reason is that they see their job as balancing the obvious (but still underappreciated) benefits of low unemployment against the risk that unemployment will get so low that workers are empowered to achieve wage increases so large that they threaten to push up inflation. They’re not wrong that falling unemployment would eventually lead to faster wage growth. A primary way that workers (especially nonunionized workers) get raises is by either leaving their current job for a better one, or threatening to leave if their bosses don’t give them a raise. When unemployment is higher, fewer better-paying jobs are out there for workers to move to, and bosses know this and don’t find threats to leave all that credible. This intuition is confirmed by data—lower unemployment is clearly associated with faster wage growth, and this effect is most pronounced for low- and moderate-wage workers with few other sources of leverage in the labor market to get raises.

{kind=link}

Defenders of the Fed’s current path would say that it makes sense when judged by the past history of the Fed—unemployment today sits below 4 percent, well below conventional estimates of the “natural” rate of unemployment that is meant to define the lowest sustainable rate of non-inflationary unemployment.

Exploring the effects of student absenteeism

With the great majority of states choosing some measurement of school attendance as their so-called “fifth metric” required by the Every School Succeeds Act,1 researchers, policymakers, and advocates are questioning how useful these metrics are at informing us about student achievement and education equity, as well as guiding policy. Indeed, while research has linked missing school to elevated risk of dropping out and poorer graduation rates, policymakers and researchers should further explore the importance of missing school, and about factors driving student absenteeism, and how to reduce it.

Our recently released report, Student absenteeism:Who misses school and how missing school matters for performance, examines how much school students are missing, which groups of students are missing the most school, and how bad missing school is for performance. We learned that about one in five students—19.2 percent—missed three or more days of school in the month before they took the 2015 National Assessment of Educational Progress (NAEP) assessment. Students who have been diagnosed with a disability, Hispanic-English language learners, Native Americans, and students who are eligible for free lunch, were the most likely to miss school, while Asian students were rarely absent. Our findings also confirmed that missing school negatively effects performance, even after accounting for student and school characteristics (including gender, race/ethnicity, language status, disability status, income, and school socioeconomic characteristics). Even students with only occasional absences were negatively affected. For these students, relative to those who did not miss school, absenteeism makes a moderate dent in their performance (a tenth of a standard deviation), but the decline in performance becomes more troubling as the number of missed days increases (up to about two-thirds of a standard deviation for those missing more than 10 school days).

Data continues to show little evidence that tax cuts are trickling down to typical workers, and now House Republicans want a do-over

In December, when Republicans passed the Tax Cuts and Jobs Act (TCJA) they chose to make tax cuts for corporations permanent, while making the individual provisions temporary to satisfy the requirements of budget reconciliation. Republicans sold these corporate tax cuts as being beneficial to everyday working people, despite the fact that previous experience gives us no reason to believe that corporate rate cuts will trickle down to anyone.

Some willing allies in the corporate world, eager to bolster the case for tax cuts, tried to hoodwink workers into believing that any bonus a worker received in 2017 was due to the TCJA. But the economic theory behind the idea that corporate rate cuts lead to higher pay for typical workers does not say that those wage increases would occur immediately (and certainly not before the tax cuts came into effect). Instead, wage bumps for workers, if they come at all, would come only after a long chain of economic events were triggered by the cut. One of the first of these events should be increased investment. We’ve long pointed out that there was reason to believe that nearly every link in this chain would break down, and that the theory itself is inconsistent with the reality of the larger deficits caused by the TCJA.

Now that the tax cuts have passed and enough time has gone by to allow some data to trickle in, is there any reason for us to change this judgement? Not really. There’s still no indication in the data that the TCJA has spurred investment—the necessary but by no means sufficient precursor to wage gains. Sure, owners of corporate shares have made out like bandits. The most recent release from the Bureau of Economic Analysis (BEA) shows that domestic after-tax corporate profits remain high, 7.5 percent of GDP in the second quarter of 2018 compared to 7.4 percent in the first quarter of 2018 and up substantially from already-high levels (6.7 percent) in 2017. Revenue collected from domestic corporate taxes remains low, 1.2 percent of GDP in the second quarter of 2018 compared to 1.1 percent in the first quarter of 2018 and 1.8 percent in 2017. Finally, undistributed domestic corporate profits – corporate profits kept internal to the firm and not distributed back to shareholders as dividends—remain historically high. This is due to the windfall the TCJA contained for multinational corporations on the profits they booked offshore. These undistributed profits (available to finance share buybacks) constituted 8.9 percent of domestic corporate gross value added in the second quarter of 2018 compared to 13.7 percent in the first quarter of 2018 and 2.6 percent in 2017. In short, the direct effects of the TCJA are here and totally visible in the data: swollen corporate profits.

Further evidence that the tax cuts have not led to widespread bonuses, wage or compensation growth

One of the leading arguments for the GOP’s Tax Cuts and Jobs Act of 2017 has been that it will raise the wages of rank-and-file workers, with congressional Republicans and members of the Trump administration promising raises of many thousands of dollars within ten years. The Trump administration’s chair of the Council of Economic Advisers argued in April that we are already seeing the positive wage impact of the tax cuts:

A flurry of corporate announcements provide further evidence of tax reform’s positive impact on wages. As of April 8, nearly 500 American employers have announced bonuses or pay increases, affecting more than 5.5 million American workers.

Following the bill’s passage, a number of corporations made conveniently-timed announcements that their workers would be getting raises or bonuses (some of which were in the works well before the tax cuts passed). But as Josh Bivens and Hunter Blair have shown there are many reasons to be skeptical of the claim that the TCJA, particularly corporate tax cuts, will produce significant wage gains.

Newly released Bureau of Labor Statistics’ Employer Costs for Employee Compensation data allow us to examine nonproduction bonuses in the first two quarters of 2018 to assess the trends in bonuses in absolute dollars and as a share of compensation. The bottom line is that there has been very little increase in private sector compensation or W-2 wages since the end of 2017. The $0.03 per hour (inflation-adjusted) bump in bonuses between the fourth quarter of 2017 and the second quarter of 2018 is very small and not necessarily attributable to the tax cuts rather than employer efforts to recruit workers in a continued low unemployment environment.

Digging into the 2017 ACS: Improved income growth for Native Americans, but lots of variation in the pace of recovery for different Asian ethnic groups

Thursday’s release of 2017 American Community Survey (ACS) data allows us to fill in the blanks for racial and ethnic groups that were not covered in Wednesday’s Census Bureau report on income, poverty, and health insurance coverage in 2017. The ACS is an annual nationwide survey that provides detailed demographic, social, and economic data for smaller populations like Native Americans and the thirteen distinct ethnic groups that make up the Asian population. (For the sake of comparability, in this blog post, the national estimates of median household income and poverty that I refer to are from the ACS.)

Between 2016 and 2017, the real median household income for Native Americans increased 3.2 percent, to $41,882. Native American median household income grew faster in 2017 than 2016 (1.8 percent), essentially bringing it back to the 2007 pre-recession level (though technically still $5 lower). Even with this boost, the median household income of Native Americans was just 69.4 percent of the national median in 2017. While this data comes from a different source than Wednesday’s data on household income and covers a slightly different survey period, it suggests that Native American median household income is similar to that of black households, but Native American households experienced much faster income growth than blacks over the last year.

Poverty declined in most states in 2017

The American Community Survey (ACS) data released today shows that the decline in the national poverty rate was felt in nearly every state. The poverty rate decreased in 42 states and the District of Columbia, with 20 of those states experiencing statistically significant declines. While there were slight increases in the poverty rate in seven states, the only statistically significant increases occurred in Delaware and West Virginia. These widespread declines are certainly good news, though most states have still not recovered to their pre-great-recession poverty rates and 40 states had higher poverty rates in 2017 than in 2000, when the economy was closer to full employment.

The national poverty rate, as measured by the ACS, fell 0.6 percentage points to 13.4 percent. This is 0.4 percentage points above the ACS poverty rate for the country in 2007, and 1.2 percentage points above the rate from 2000.

Between 2016 and 2017, the District of Columbia saw the largest decline in its poverty rate (-2.0 percentage points), followed by Idaho (-1.6 percentage points), Arizona (-1.5 percentage points), Maine (-1.4 percentage points), Kentucky (-1.3 percentage points), and Rhode Island (-1.2 percentage points). There were increases in poverty in Delaware (1.9 percentage points), West Virginia (1.2 percentage points), Alaska (1.2 percentage points), New Hampshire (0.4 percentage point), Hawaii (0.2 percentage point), South Carolina (0.1 percentage point), and Massachusetts (0.1 percentage point). In Wyoming, the rate remained essentially unchanged between 2016 and 2017.Read more

Household incomes in 2017 stayed on existing trends in most states; incomes in 21 states are still below their pre-recession levels

The state income data for the American Community Survey (ACS), released this morning by the Census Bureau, showed that in 2017, household incomes across the states stayed largely on the same trajectories that they were heading in 2016, with a handful of exceptions. From 2016 to 2017, inflation-adjusted median households incomes grew in 40 states and the District of Columbia (24 of these changes were statistically significant.) The ACS data showed an increase of 2.5 percent increase in the inflation-adjusted median household income for the country as a whole—an increase of $1,492 for a typical U.S. household. Despite these increases, households in 21 states still had inflation-adjusted median incomes in 2017 below their 2007 pre-recession values.

From 2016 to 2017, the largest percentage gains in household income occurred in the District of Columbia, where the typical household experienced an increase of $5,258 in their annual income—an increase of 6.8 percent. With this increase, the District of Columbia now has the highest median household income in the country at $82,372—though comparing D.C. to states is problematic, since D.C. is a city, not a state. Maryland remains the state with the highest median household income at $80,776—a value essentially unchanged (0.2 percent growth) from 2016 to 2017. Households in 13 states experienced growth faster than the U.S. average of 2.5 percent: Montana (4.5 percent), Maine (3.8 percent), California (3.8 percent), Washington (3.6 percent), Tennessee (3.5 percent), Arizona (3.4 percent), Rhode Island (3.2 percent), Nebraska (3.1 percent), Colorado (3.0 percent) New Jersey (3.0 percent), Nevada (2.9 percent), Virginia (2.8 percent), and Georgia (2.7 percent).Read more

Government programs kept tens of millions out of poverty in 2017

From 2016 to 2017, the official poverty rate fell by 0.4 percentage points, as household income rose modestly, albeit unevenly, throughout the income distribution. This was the third year in a row that poverty declined, but the poverty rate remains a full percentage point higher than the low of 11.3 percent it reached in 2000.

Since 2010, the U.S. Census Bureau has also released an alternative to the official poverty measure known as the Supplemental Poverty Measure (SPM).1

The SPM corrects many potential deficiencies in the official rate. For one, it constructs a more realistic threshold for incomes families need to live free of poverty, and adjusts that threshold for regional price differences. For another, it accounts for the resources available to poor families that are not included in the official rate, such as food stamps and other in-kind government benefits.

As shown in Figure A, a larger proportion of Americans are in poverty as measured by the SPM than the official measure reports. (Importantly, however, researchers who constructed a longer historical version of the SPM found that it shows greater long-term progress in reducing poverty than the official measure.) In 2017, the SPM declined by 0.1 percentage points to 13.9 percent. Under the SPM, 45.0 million Americans were in poverty last year, compared with 39.7 million Americans under the “official” poverty measure.

10 years after the start of the Great Recession, black and Asian households have yet to recover lost income

Today’s Census Bureau report on income, poverty, and health insurance coverage in 2017 shows that while all race and ethnic groups shared in the growth in median household incomes during the previous two years, that trend abruptly ended for African American households in 2017. Real median incomes were basically flat among African Americans (from $40,339 to $40,258) and down among Asians (from $83,182 to $81,331), but up 3.7 percent (from $48,700 to $50,486) among Hispanics, and 2.6 percent (from $66,440 to $68,145) among non-Hispanic whites. The decline in Asian household incomes was not statistically significant. As a result of stalled income growth among African Americans, recent progress in closing the black-white income gap over the last couple years has been reversed. The median black household earned just 59 cents for every dollar of income the white median household earned (down from 61 cents), while the median Hispanic household earned just 74 cents (up from 73 cents). Meanwhile, households headed by persons who are foreign-born saw little change in median incomes between 2016 and 2017 (from $56,754 to $57,273), compared to an increase of 1.5 percent (from $61,066 to $61,987) among households with a native-born household head.Read more

Black workers have made no progress in closing earnings gaps with white men since 2000

This week, the Census Bureau released its report on incomes, earnings, and poverty rates for 2017. Most analysis has paid particular attention to the changes between 2016 and 2017, but this post takes a deeper look at earnings by race and gender over a longer period of time—since 2000—to paint a more complete picture of what has happened over the last full business cycle (2000-2007) plus the most recent recession and recovery (2007-2017). Since 2000, wages have been generally stagnant, and large gaps persist by race and gender, despite an expanding and increasingly productive economy.

To a great extent, trends in annual earnings since 2000 resemble the overall wage stagnation we’ve seen since the mid-1970s. (Here, we discuss annual full time earnings, but the long-run trends are consistent with the hourly wage data. For an extensive discussion of hourly wage trends, see The State of American Wages 2017.) Between 2016 and 2017, full-time year-round men’s and women’s earnings fell 1.1 percent. Men’s median earnings are still 1.9 percent below their 2000 level, while women’s earnings are now 7.1 percent higher than in 2000. Because of these divergent trends, the overall gender wage gap narrowed between 2000 and 2017, though at a slower rate than in the previous two decades.

These patterns in men’s and women’s full-time median annual earnings can be further broken down by race. As you can see in the figure below, real median earnings of full-time workers—male and female, black and white—have been relatively flat since 2000. Unlike the previous year’s data where only white women saw a significant increase in median earnings, only white men saw their median wages rise between 2016 and 2017. For the most part, median wages were flat or falling in the full business cycle of 2000–2007, and black men have still not grown past their 2000 levels.

Household income growth slowed markedly in 2017 and was stronger for those at the top, while earnings declined slightly

Today’s report from the Census Bureau shows a marked slowdown in median household income growth relative to previous years. Median household incomes rose 1.8 percent, after an impressive 5.1 percent gain in 2015 and a 3.1 percent gain in 2016; median non-elderly household income saw a similar rise of 2.5 percent this year after gaining 4.6 percent and 3.6 percent in the prior two years, respectively. However, inflation-adjusted full-time annual earnings for both men and women fell by 1.1 percent in 2017. Men’s earnings are still below their 2007 level (by 2.5 percent points), while women’s earnings are now 0.9 percent above. This year’s report is hence a bit discouraging; earnings for low and middle-income workers need to make strong and sustained gains if we are to have an economy that works for typical American households and not just for the well-off.

While the gains in household income are markedly slower than in previous years, they nonetheless represent another small step toward reclaiming the lost decade of income growth caused by the Great Recession. Part of this year’s slowdown in income growth relative to 2016 is likely driven by a small increase in the pace of inflation. In 2017, year-over-year inflation was 2.2 percent compared to 1.3 percent in 2016. However, as discussed below, this year’s report reminds us that the vast majority of household incomes (when corrected for a break in the data series in 2013) have still not fully recovered from the deep losses suffered in the Great Recession.

Non-elderly household incomes improve

The Census data show that from 2016–2017, inflation-adjusted median household incomes for non-elderly households (those with a head of household younger than 65 years old) increased 2.5 percent, from $67,917 to $69,628. Median non-elderly household income is an important measure of an improving economy, as those households depend on labor market income for the vast majority of their income. This continued, albeit slower, increase after large gains in the prior two years is a welcome trend. Median household income for non-elderly households, which finally recovered to its pre-recession level in 2017, was 0.8 percent, or $530, above its level in 2007. It’s important to note that the Great Recession and its aftermath came on the heels of a weak labor market from 2000–2007, during which the median income of non-elderly households fell significantly, from $71,577 to $69,098—the first time in the post-war period that incomes failed to grow over a business cycle. Altogether, from 2000–2017, the median income for non-elderly households fell from $71,577 to $69,628, a decline of $1,949, or 2.7 percent. In short, the last three years should not make us forget that incomes for the majority of Americans have experienced a lost 17 years of growth.Read more

By the Numbers: Income and Poverty, 2017

Jump to statistics on:

• Earnings

• Incomes

• Poverty

• Policy / SPM

This fact sheet provides key numbers from today’s new Census reports, Income and Poverty in the United States: 2017 and The Supplemental Poverty Measure: 2017. Each section has headline statistics from the reports for 2017, as well as comparisons to the previous year, to 2007 (the final year of the economic expansion that preceded the Great Recession), and to 2000 (the historical high point for many of the statistics in these reports.) All dollar values are adjusted for inflation (2017 dollars).

Earnings

Median annual earnings for men working full time fell 1.1 percent, to $52,146, in 2017. Men’s earnings are down 2.5 percent since 2007, and are still 1.9 percent lower than they were in 2000.

Median annual earnings for women working full time fell 1.1 percent, to $41,977, in 2017. Women’s earnings are up 0.9 percent since 2007, and are 7.1 percent higher than they were in 2000.

Median annual earnings for men working full time in 2017: $52,146

Change over time:

- 2016–2017: -1.1%

- 2007–2017: -2.5%

- 2000–2017: -1.9%

Median annual earnings for women working full time in 2017: $41,977

Change over time:

- 2016–2017: -1.1%

- 2007–2017: 0.9%

- 2000–2017: 7.1%

What to watch for in the 2017 Census data on earnings, incomes, and poverty

Next Wednesday is the Census Bureau’s release of annual data on earnings, income, poverty, and health insurance coverage for 2017, which will give us a picture of the economic status of working families 10 years since the start of the Great Recession—and in the first year of the Trump presidency. Next week’s release will help us chart the progress made by the typical American household in clawing back nearly two decades of lost income growth—the result of a failure of incomes to return to the business cycle peaks of 2000 during the slow early-2000s recovery and expansion, and the Great Recession. We’ll be paying particular attention to differences in the recovery across racial and ethnic groups.

What happened with incomes in 2016?

After adjusting the series to account for changes to the survey in 2013, 2016 median incomes for American households fell just shy of their pre-Great Recession peaks, even after two years of impressive across-the-board improvements (as shown in the figure below). It is important to note, however, that some of the improvements in inflation-adjusted income we saw in 2015 and 2016 were driven by atypically low inflation—0.1 percent in 2015, and 1.3 percent in 2016. While we don’t expect a similar boost from low inflation in 2017 (inflation increased 2.2 percent in 2017), we anticipate that an additional year of even modest growth will likely bring the broad middle class back to pre-recession incomes. But, for non-elderly households, the latest data will be likely still below the peak reached 17 years prior.

Real median household income, all and non-elderly, 1995–2016

| All households | All households- imputed series | All households- new series | Non-elderly households | Non-elderly households- imputed series | Non-elderly households- new series | |

|---|---|---|---|---|---|---|

| 1995 | $53,330 | $55,020 | $61,268 | $63,173 | ||

| 1996 | $54,094 | $55,808 | $62,399 | $64,338 | ||

| 1997 | $55,207 | $56,956 | $63,203 | $65,168 | ||

| 1998 | $57,223 | $59,036 | $65,775 | $67,820 | ||

| 1999 | $58,647 | $60,506 | $67,451 | $69,548 | ||

| 2000 | $58,525 | $60,380 | $67,783 | $69,890 | ||

| 2001 | $57,248 | $59,062 | $66,737 | $68,811 | ||

| 2002 | $56,591 | $58,384 | $66,066 | $68,120 | ||

| 2003 | $56,522 | $58,313 | $65,464 | $67,499 | ||

| 2004 | $56,333 | $58,118 | $64,705 | $66,717 | ||

| 2005 | $56,947 | $58,752 | $64,275 | $66,273 | ||

| 2006 | $57,390 | $59,208 | $65,159 | $67,184 | ||

| 2007 | $58,150 | $59,993 | $65,457 | $67,492 | ||

| 2008 | $56,079 | $57,856 | $63,311 | $65,280 | ||

| 2009 | $55,689 | $57,454 | $62,451 | $64,392 | ||

| 2010 | $54,242 | $55,961 | $60,847 | $62,738 | ||

| 2011 | $53,413 | $55,106 | $59,374 | $61,220 | ||

| 2012 | $53,335 | $55,025 | $59,959 | $61,823 | ||

| 2013 | $53,513 | $55,209 | $55,209 | $60,220 | $62,092 | $62,092 |

| 2014 | $54,404 | $61,304 | ||||

| 2015 | $57,231 | $64,146 | ||||

| 2016 | $59,039 | $66,487 | ||||

Note: Because of a redesign in the CPS ASEC income questions in 2013, we imputed the historical series using the ratio of the old and new method in 2013. Solid lines are actual CPS ASEC data; dashed lines denote historical values imputed by applying the new methodology to past income trends. Non-elderly households are those in which the head of household is younger than age 65. Shaded areas denote recessions.

Source: EPI analysis of Current Population Survey Annual Social and Economic Supplement Historical Income Tables (Tables H-5 and HINC-02)

What do we expect in this year’s release?

Given the data we’ve seen for 2017 from other sources, it is likely that earnings, income, and poverty in the 2017 Census data will show some improvement over the past year. But it is also likely that this pace of improvement will be significantly slower than the previous two years’ growth. As the economy steadily strengthens, we’ve seen progress in key labor market indicators, including participation in the labor market and payroll employment, which should boost household labor earnings. However, hourly wage data suggest that wage growth in 2017 continues to be unequal and slower than expected at this point in the business cycle. In 2017, strong growth in hourly wages continued at the top (1.5 percent at the 95th percentile), while the 10th percentile saw the strongest growth at 3.7 percent due in part to a tightening labor market as well as state-level minimum wage increases. However, median wages grew only 0.2 percent.Read more

What to Watch on Jobs Day: Keeping a cautiously optimistic eye on wages

Nominal wage growth has been slower than would be expected over the last year, particularly in light of an unemployment rate hovering around 4.0 percent. In a tight labor market, employers should be finding it harder and harder to attract and retain the workers they want—and, therefore they should be raising wages in order to get them. But, that’s not happening enough to move the dial on wage growth. In this preview post for jobs day, I’m going to review some reasons that do NOT explain slower wage growth, then discuss some far more compelling explanations.

In the last several weeks, some colleagues and I tried to dispel a few myths about why wages aren’t rising as fast as would be expected in this labor market. One reason wage growth could be slow is if lower wage jobs are being added at a disproportionate rate, but the composition of new jobs is not what is keeping wage growth so sluggish right now. Instead, we are simply seeing sluggish wage growth within a wide variety of job-types. Some have posited that our far-less-than-stellar wage growth right now could be due to workers not having the skills employers need. But that idea has the logic backwards. When employers can’t find workers with the skills they need at the wages they are offering, they will raise wages in order to attract qualified workers—if employers can’t find the workers they need among the unemployed, they will offer higher wages in an attempt to poach needed workers from other firms, who will then raise wages in an attempt to keep their workers, and so on. In other words, if there are skills shortages, we should see signs of faster wage growth for workers with needed skills. This fast wage growth for skilled workers should push up average wages, not weigh them down. Furthermore, if there was a credential shortage, we’d expect faster wage growth among those with more credentials, which has also not been happening in the past couple of years.

So, then what is it? One reason why employers may not feel compelled as of yet to raise wages is that the unemployment rate is overstating the strength of the labor market. There are still sidelined workers—not counted in the unemployment rate—who are returning to the labor market month after month in search of, and, in many cases, finding jobs. The simple fact of these would-be workers out there lowers the leverage today’s workers have to see faster wage growth from their employers.

Separate is still unequal: How patterns of occupational segregation impact pay for black women

August 7th is Black Women’s Equal Pay Day, the day that marks how long into 2018 an African American woman would have to work in order to be paid the same wages her white male counterpart was paid last year. On average, in 2017, black women workers were paid only 66 cents on the dollar relative to non-Hispanic white men, even after controlling for education, years of experience, and geographic location. A previous blog post dispels many of the myths behind why this pay gap exists, including the idea that the gap would be closed by black women getting more education or choosing higher paying jobs. In fact, black women earn less than white men at every level of education and even when they work in the same occupation. But even if changing jobs were an effective way to close the pay gap black women face—and it isn’t—more than half would need to change jobs in order to achieve occupational equity.

Figure A plots the “Duncan Segregation Index” (DSI) for black women and white men, overall and by education, based on individual occupation data from the American Community Survey (ACS). This is a common measure of occupational segregation, which, in this case identifies what percentage of working black women (or white men) would need to change jobs in order for black women and white men to be fully integrated across occupations. Values of the DSI can range from 0 percent (complete integration) to 100 percent (complete segregation).

As shown in Figure A, there has been little progress on reducing occupational segregation between black women and white men since 2000. From 2000 to 2016 (latest data year available), the DSI only changed from 59 percent to 56 percent. This means that on average, 56 percent of black women (or white men) would need to change occupations in order to achieve occupational equity, or full integration of these two groups in the workforce.

How do we know the tax cut isn’t working to boost wages? Investment, investment, investment

Earlier this week, my colleague Hunter Blair noted that economic data released over the past six months contained no real signs that any of the promised benefits of the Republican tax cut passed at the end of last year were showing up for workers. These benefits are certainly showing up for corporations and the wealthy households that own them—which makes sense, as the tax cut was overwhelmingly a tax cut for corporations. But the tax cut’s boosters promised that money corporations saved on taxes would quickly show up as higher wages for workers. In fact, they claimed this was happening so quickly that the tax cut was responsible for bonuses at the end of 2017 that were granted or announced before the tax cut actually became law.

As silly as those arguments were, a case that corporate tax cuts will lead to wage increases does exist in economics textbooks. The most crucial link in the chain leading from cutting corporations’ taxes to workers seeing higher paychecks runs through increased business investment in plants, equipment, and research. Essentially, lower corporate taxes are supposed to incentivize businesses to undertake more investment in productivity-enhancing plants, equipment, and research, and induce extra spending to finance these increased investments. This extra investment is supposed to lead to higher productivity, and hence to higher wages for workers. I should note that most of the links in this chain are broken, but for now, let’s just focus on the first—the effect of the tax cut in spurring business investment. If that fails, the whole case for tax cuts boosting wages fails.

The figure below shows the percent change in business investment relative to the same quarter in the previous year, with the vertical line showing when the tax cut was passed. The data is from the Bureau of Economic Analysis (BEA), National Income and Product Accounts (NIPA) Table 1.1.3. It is awfully hard to see a real regime change here in investment behavior.

What to Watch on Jobs Day: Wringing out every last bit of slack in the labor market

Two weeks ago, EPI released a paper by Estelle Sommeiller and Mark Price detailing, county-by-county, the rise in income inequality since the 1970s. Since the Great Recession, the top 1 percent of families have captured 41.8 percent of all income growth in the United States—and this disproportionate hoarding of economic growth is not unique to East Coast metropolises and Silicon Valley. All across the country, downward pressure on wages and incomes for most Americans has limited their ability to benefit from a growing economic pie. A decline in unionization and other deliberate policy choices that have reduced typical workers’ leverage and bargaining power in the labor market have contributed to these worrying trends.

Nonetheless, some experts still question why today’s relatively tighter economy isn’t bringing benefits to workers in the form of increased wages, given that we’ve seen relatively low unemployment rates over the course of the past two years—below 4.5 percent unemployment since March of last year. Josh Bivens reiterated this week EPI’s consistent stance that, “weak wage growth should make us think that by definition there is still slack in the labor market, and this might mean rethinking just how low unemployment can go.” Given this reality, policymakers (including the Fed) should stop attempting to slow the economy and allow the labor market to keep tightening, until there is consistent evidence that the benefits of a strong economy are being shared with a wide swath of the workforce. This includes many women of color who face pay gaps so large that they typically would need to work through the third or fourth quarter of another year just to earn as much as the average white man earned during the previous year. For black women, that date is next Tuesday, August 7.

In last month’s jobs report, we saw the unemployment rate tick up from 3.8 to 4.0, for positive reasons. The rise was accompanied by an increase in labor force entrants, suggesting workers are feeling optimistic about the jobs market and sidelined workers are indeed still being drawn back into the labor force. Looking at today’s prime-age employment-to-population ratio, which is still below the peaks of the last two business cycles, this is less surprising. As it has for most of the past several years, the low unemployment rate looks to be potentially overstating the strength of the labor market.

Tomorrow morning, we will continue to look at the unemployment rate, given its recent volatility, but we will also be watching nominal wage growth and the prime-age employment-to-population ratio for evidence that the economy continues to move closer to full employment.

The “wage puzzle” is real—but low inflation and low productivity are also puzzles that need to be solved

Jason Furman’s recent piece in Vox is drawing lots of comments (including one by me on a relatively minor issue). The last couple of months have seen lots of attention focused on relatively weak wage growth even in the face of low unemployment—sometimes referred to as the “wage puzzle.” I and others have argued that this weak wage growth should make us think that by definition there is still slack in the labor market, and this might mean rethinking just how low unemployment can go. Furman argues instead that wage growth is not that low, and that labor markets are tight indeed. A main piece of evidence he highlights to support this view is that both inflation and productivity growth have been low in recent years, and, adjusted for these two influences we really can’t expect wage growth to be any higher than it has been.

Furman is quick to note that his outlook does not demand rapid policy tightening to rein in growth. I’m definitely happy he says this. However, I do think any argument that concludes that the U.S. economy is unambiguously at full employment, and that the labor market is even tighter than the late 1990s, is going to give succor to those calling for the Federal Reserve to continue raising interest rates briskly to rein in growth.

This would be a mistake, and Furman’s arguments should certainly not sway anybody to call for continued policy tightening. He makes some good points, but I think he misreads what low inflation and low productivity are telling us. They are not just background variables that we have to take as given and adjust our wage expectations accordingly. Instead, low inflation and low productivity should be seen as signs of slack in and of themselves.

Last week’s GDP data shows there’s still no reason to think the TCJA’s corporate rate cuts are trickling down to workers

Last Friday, new data was released by the Bureau of Economic Analysis (BEA) with the headline being a 4.1 percent annualized rate of GDP growth. Supporters of the Tax Cuts and Jobs Act (TCJA) have pointed to this data point as proof that the tax cuts are working, though there’s little indication that economic growth has moved off its previous trend. But the release of new economic data does give us another chance to see what that data is telling us so far about the effects of the TCJA. The punchline is simple: the TCJA has already fattened up the incomes of capital owners and corporations in a measurable way, but there’s no indication at all that any of it threatens to trickle-down to workers.

The corporate sector is unsurprisingly where the clearest near-term effects of the TCJA can be seen. Domestic after-tax corporate profits increased from 6.7 percent of GDP in 2017 to 7.4 percent in the first quarter of 2018. In particular, undistributed domestic corporate profits surged in response to the TCJA’s tax windfall for multinational corporations on the profits they had booked offshore. As the chart below shows, much like the spike following the 2004 repatriation tax “holiday,” undistributed domestic corporate profits rose from 2.5 percent of gross domestic corporate value added in 2017 to 12 percent in the first quarter of 2018. We should note that 2004’s tax holiday didn’t lead to a surge in wage growth in subsequent years.

First quarter data from 2018 shows an enormous spike in undistributed profits: Undistributed domestic corporate profits as a percent of domestic corporate gross value added, 1979Q1-2018Q1

| Undistributed profits as a percent of corporate gross value added | |

|---|---|

| 1979Q1 | 4.71% |

| 1979Q2 | 4.39% |

| 1979Q3 | 4.05% |

| 1979Q4 | 3.70% |

| 1980Q1 | 2.84% |

| 1980Q2 | 1.73% |

| 1980Q3 | 2.42% |

| 1980Q4 | 3.02% |

| 1981Q1 | 3.30% |

| 1981Q2 | 3.57% |

| 1981Q3 | 4.13% |

| 1981Q4 | 3.74% |

| 1982Q1 | 3.15% |

| 1982Q2 | 4.05% |

| 1982Q3 | 3.70% |

| 1982Q4 | 3.05% |

| 1983Q1 | 3.35% |

| 1983Q2 | 3.88% |

| 1983Q3 | 4.08% |

| 1983Q4 | 4.39% |

| 1984Q1 | 5.08% |

| 1984Q2 | 5.02% |

| 1984Q3 | 5.17% |

| 1984Q4 | 5.39% |

| 1985Q1 | 5.15% |

| 1985Q2 | 4.77% |

| 1985Q3 | 5.37% |

| 1985Q4 | 4.36% |

| 1986Q1 | 3.72% |

| 1986Q2 | 3.08% |

| 1986Q3 | 2.83% |

| 1986Q4 | 2.34% |

| 1987Q1 | 2.62% |

| 1987Q2 | 2.98% |

| 1987Q3 | 3.45% |

| 1987Q4 | 3.18% |

| 1988Q1 | 3.80% |

| 1988Q2 | 3.43% |

| 1988Q3 | 2.91% |

| 1988Q4 | 3.62% |

| 1989Q1 | 2.09% |

| 1989Q2 | 2.15% |

| 1989Q3 | 2.13% |

| 1989Q4 | 1.75% |

| 1990Q1 | 1.48% |

| 1990Q2 | 1.81% |

| 1990Q3 | 1.01% |

| 1990Q4 | 0.92% |

| 1991Q1 | 1.49% |

| 1991Q2 | 1.57% |

| 1991Q3 | 1.59% |

| 1991Q4 | 1.31% |

| 1992Q1 | 1.54% |

| 1992Q2 | 1.50% |

| 1992Q3 | 1.36% |

| 1992Q4 | 1.66% |

| 1993Q1 | 1.53% |

| 1993Q2 | 1.99% |

| 1993Q3 | 2.30% |

| 1993Q4 | 2.54% |

| 1994Q1 | 3.09% |

| 1994Q2 | 3.24% |

| 1994Q3 | 3.40% |

| 1994Q4 | 3.55% |

| 1995Q1 | 3.30% |

| 1995Q2 | 3.46% |

| 1995Q3 | 3.71% |

| 1995Q4 | 3.75% |

| 1996Q1 | 4.14% |

| 1996Q2 | 4.04% |

| 1996Q3 | 3.91% |

| 1996Q4 | 3.97% |

| 1997Q1 | 4.25% |

| 1997Q2 | 4.20% |

| 1997Q3 | 4.38% |

| 1997Q4 | 3.92% |

| 1998Q1 | 2.83% |

| 1998Q2 | 2.85% |

| 1998Q3 | 3.16% |

| 1998Q4 | 2.69% |

| 1999Q1 | 3.04% |

| 1999Q2 | 2.94% |

| 1999Q3 | 2.57% |

| 1999Q4 | 1.82% |

| 2000Q1 | 1.37% |

| 2000Q2 | 1.08% |

| 2000Q3 | 0.87% |

| 2000Q4 | 0.46% |

| 2001Q1 | 0.57% |

| 2001Q2 | 1.00% |

| 2001Q3 | 0.33% |

| 2001Q4 | -0.29% |

| 2002Q1 | 1.38% |

| 2002Q2 | 1.56% |

| 2002Q3 | 2.06% |

| 2002Q4 | 2.36% |

| 2003Q1 | 2.66% |

| 2003Q2 | 1.88% |

| 2003Q3 | 2.66% |

| 2003Q4 | 2.41% |

| 2004Q1 | 2.92% |

| 2004Q2 | 3.34% |

| 2004Q3 | 3.51% |

| 2004Q4 | 1.22% |

| 2005Q1 | 3.24% |

| 2005Q2 | 4.83% |

| 2005Q3 | 6.26% |

| 2005Q4 | 8.40% |

| 2006Q1 | 3.79% |

| 2006Q2 | 3.40% |

| 2006Q3 | 3.22% |

| 2006Q4 | 1.40% |

| 2007Q1 | 2.11% |

| 2007Q2 | 2.38% |

| 2007Q3 | 0.99% |

| 2007Q4 | 1.16% |

| 2008Q1 | 0.88% |

| 2008Q2 | 0.66% |

| 2008Q3 | 2.14% |

| 2008Q4 | 1.91% |

| 2009Q1 | 1.01% |

| 2009Q2 | 1.53% |

| 2009Q3 | 3.22% |

| 2009Q4 | 3.84% |

| 2010Q1 | 4.38% |

| 2010Q2 | 4.73% |

| 2010Q3 | 5.10% |

| 2010Q4 | 4.57% |

| 2011Q1 | 3.40% |

| 2011Q2 | 4.51% |

| 2011Q3 | 4.52% |

| 2011Q4 | 4.69% |

| 2012Q1 | 4.49% |

| 2012Q2 | 4.78% |

| 2012Q3 | 4.17% |

| 2012Q4 | 2.56% |

| 2013Q1 | 4.60% |

| 2013Q2 | 4.71% |

| 2013Q3 | 3.49% |

| 2013Q4 | 4.75% |

| 2014Q1 | 2.65% |

| 2014Q2 | 3.81% |

| 2014Q3 | 4.97% |

| 2014Q4 | 4.75% |

| 2015Q1 | 3.63% |

| 2015Q2 | 3.37% |

| 2015Q3 | 3.65% |

| 2015Q4 | 2.47% |

| 2016Q1 | 3.33% |

| 2016Q2 | 2.18% |

| 2016Q3 | 2.48% |

| 2016Q4 | 2.00% |

| 2017Q1 | 2.17% |

| 2017Q2 | 2.24% |

| 2017Q3 | 3.06% |

| 2017Q4 | 2.58% |

| 2018Q1 | 12.04% |

Source: EPI analysis of data from table 1.14 from the National Income and Product Accounts (NIPA) from the Bureau of Economic Analysis (BEA).

Corporate tax revenues as a share of the economy fell by more than a third, from 1.8 percent of GDP in 2017 to 1.1 percent in the first quarter of 2018. This data makes it clear that the TCJA made some people very rich in the first quarter of 2018. (Second quarter corporate data has not been released yet.) Does Friday’s data on the overall economy show any indication that the corporate tax cuts have started to trickle down to workers as the Trump administration promised?

Nope, not at all. For one, wages haven’t budged. To be fair, no serious economist should have argued that wages are expected to respond immediately to corporate tax cuts. Though that didn’t keep TCJA supporters (including some economists willing to act unserious) from touting bonuses paid late last year as proof that the tax cuts were working as intended. It’s worth reminding ourselves of the economic chain of causation that leads from corporate tax cuts to wage growth. First, the direct benefits of corporate tax cuts flow entirely to shareholders. That part has definitely happened. Then, (as we’ve previously explained), higher after-tax profitability is supposed to incentivize firms to invest more, with those investments financed by the higher savings that households provide in response to higher returns. These investments in turn are supposed to give workers more and better tools to do their jobs, which boosts productivity and eventually that increase in productivity translates into wage growth.

Nothing misleading about this: Typical workers’ pay and productivity have diverged

Jason Furman has an interesting piece on Vox today, claiming that the “puzzle” of weak wage growth in the face of low unemployment is not really a puzzle at all.

There’s a lot in this piece to agree with and a lot to quibble with. But, this post will just note one quick quibble. Furman describes a chart of ours—one we like a lot—as “misleading.” Here’s the full paragraph from him:

Productivity does a good job of explaining the evolution of average wage growth in the United States as well, especially prior to 2000. (But it does a decent job even since then, even with the wage slowdown.) From the end of World War II until around 2000 average wages grew almost lock-step with productivity — if you use the same measure of inflation for both concepts, so the comparison is apples to apples. Often, presentations of the comparison between wages and productivity, as in this much-reproduced graphic, use a higher inflation measure to adjust wages than productivity and thus produce a misleading impression.

This is a criticism we’ve seen, and addressed, before, so forgive me if I seem a tad sensitive on this, but I want to be really clear: there is nothing misleading about our presentation of this data. The wedge we show between our measure of pay and economy-wide productivity is indeed driven overwhelmingly by rising inequality and not the differing deflators. In this figure we measure the pay of typical workers, not average wages. We define “typical” as either the median worker (the one in the middle of the wage distribution) or the average pay of production and non-supervisory workers (a group consisting of about 80 percent of the private-sector workforce). We don’t use average pay precisely because, as Jason notes, average pay kept up pretty well with economy-wide productivity pre-2000. This means that the bulk of the rise in inequality over that time was driven by inequality within wages, or the divergence between average and typical pay (as we clearly show—see the previous link).

{kind=link}

Does America’s monopoly problem mean that high-pressure labor markets can’t boost wages?

Last week, I wrote a piece on why the erosion of workers’ labor market leverage does not imply that genuine full employment won’t be accompanied by wage growth. It was in response to questions about why wages in the United States weren’t growing faster given that unemployment is pretty low in historical terms. The punchline of the discussion was pretty clear: the definition of full employment is wages rising fast enough to put upward pressure on the Federal Reserve’s inflation target. If wages aren’t rising this fast, then we aren’t at full employment. The eroding relative labor market leverage power of workers does not change this.

Another reason often given for slow wage growth in the face of relatively low unemployment is rising monopolization. Does monopoly change any of the calculus I sketched out above? Almost surely not.

To be really clear on this, I’m more-than-sympathetic to the view that the U.S. economy has a monopoly problem. Empirical research clearly shows upticks in industry concentration ratios, and a number of large and crucial economic sectors (health care and finance, in particular) are characterized by immense pricing power of producers. Other sectors (mostly technology) have also seen waves of consolidation that have not led (yet?) to rapid price growth, but have raised a whole host of concerns about the intersection of economic and political power.